Huhu... US to Open Criminal Inquiry into Goldman Trading

One of the most interesting posting on Goldman Sachs case was highlighted on Zero Hedge.

The posting is called The Mainstream Media Doesn’t Know Sh*t About Securities Law or the Goldman Case

Do give it a read. :D

Friday, April 30, 2010

Goldman Case: Do You Know Or Do You Not Know?

Reply To Notion's EPS Dilution Caused By Share Placements

Got the following reply on my posting Honey, My Notion's Earnings Per Share Has Shrunk!

- Shien Yang said...

Hi there,the EPS is definitely going to get diluted this year. But u need to understand what the private placement is for. They need the money for the huge capex that they are going to incur this year for their capacity expansion.

The result for all these money spent u will see it in FY11 when their net profit will jump again due to more than 3x increase in their production capacity for HDD parts.

Hello.

Regarding what the private placement is for... err.. well, I could actually write something like this ....

Let's have a look at recent events. ( Ok, I won't stretch it so far back.)

Let's look and assume that one bought Notion in mid Nov 2009. Why? Based on impressive earnings.

This was the earnings announced on 10th Nov 2009. Quarterly rpt on consolidated results for the financial period ended 30/9/2009

Notion then reported a sales revenue of 54.339 million and an earnings of 13.029 million. Previous quarter it made some 11.087 million only. An impressive jump in earnings.

Earnings then was based on 703.583 million shares.

In the very same month, Notion did a share consolidation. 5 into 1. Meaning the number of shares will be consolidated into 140.717 million shares.

Notion has 20.470 million in its cash balances and some 58.274 million in total loans.

The share placement of 10% was announced a month earlier. Announcement - Proposed Private Placement.pdf

Rationale of the placement explained in the pdf link above.

- NVB announced on 2 October 2009 that its wholly-owned subsidiary, Notion (Thailand) Co. Ltd has entered into an agreement to acquire a parcel of land with a factory located thereon. The proceeds from the Proposed Private Placement will be utilised for the extension of the existing factory, purchase of machinery and to defray expenses incidental to the Proposed Private Placement. The plant in Thailand is expected to commence operations during the 1st quarter of 2010.

After due consideration of the various methods of fund raising, the Board is of the view that the Proposed Private Placement is currently the most appropriate method of fund-raising as it would enable the Company to raise the funds required which would otherwise have to be financed through bank borrowings thereby resulting in interest savings to NVB and its subsidiaries (“Group”).

And then on 19th Jan 2010. NOTION VTEC BERHAD (“NVB” or “Company”) Private placement of up to ten percent (10%) of the issued and paid-up share capital of the Company (“Private Placement”)

- HwangDBS Investment Bank Berhad, on behalf of the Board of Directors of NVB (“Board”), wishes to announce that the Private Placement has been completed with the listing of 13,844,694 new ordinary shares of RM0.50 each in NVB (“Placement Shares”) on the Main Market of Bursa Malaysia Securities Berhad on 18 January 2010. The Placement Shares were placed to Nikon Corporation (“Nikon”), which has a global standing in the manufacture and sale of camera-related products, such as digital cameras, as well as binoculars and other optical products for consumers, such as ophthalmic lenses.

Nikon Corporation was the buyer of the placement of shares.

The placement raised...

- The proceeds raised approximately RM33.78 million.

And the strange thing was ...

- The proceeds raised approximately RM33.78 million which will be used for the NVB Group’s expansion plans in Thailand which will add an extra floor space of 200,000 sq ft to the Group's facilities and defraying expenses incidental to the Private Placement. The Thailand plant will, in the initial stage, mainly cater for Nikon (Thailand) Co Ltd which has indicated that there will be more orders for the cam barrels and possible sub assemblies in the near future.

So Notion Vtec placed 10% shares to Nikon and the proceeds is then used in Notion's expansion plans in Thailand. This adds an extra floor space of 200,000 square feet. And this expansion caters for Nikon's orders.

Feb 2010, Notion announced this earnings. Quarterly rpt on consolidated results for the financial period ended 31/12/2009

On a q-q basis, sales increased from 54.339 million to 56.329 million. Net earnings improved from 13.029 million to 14.185 million.

Yesterday's earnings. Notion's sales were rather flat at 56.709 million. Net earnings slipped to 12.522 million.

The cash raised from Notion's placement to Nikon can be seen in Notion's cash balances indicating clearly that Notion had yet to deploy the proceed from its placement to Nikon. Which is understandable.

Now the rationale of the placement yesterday.

- The Placement Shares are intended to be placed out to long-term institutional investors and/or strategic investors and will enable NVB to raise gross proceeds of up to RM46.06 million (based on the indicative issue price per Placement Share of RM2.98) to fund future capital expenditure for its centralised 2.5” HDD baseplate manufacturing facility in Klang, working capital and to defray expenses incidental to the Proposals. The Board is of the view that the Proposed Private Placement is the most appropriate method of raising funds as the funds required would otherwise have to be financed through bank borrowings which would result in the NVB Group incurring interest cost.

So two placements. One to Nikon and another in the works.

How?

Now all that would have been extremely tedious and so long winded, yes? :D

So for your question on whether I do understand what the private placements for. Well I do understand and I did read Notion Vtec's explanation for the need of the placement of shares.

Frankly, IF I were a shareholder, I would have preferred a rights issue, where all the minority shareholders are given an EQUAL and FAIR chance to participate in the company's expansion program. Yes, if all the minority shareholders reckon that the expansion plans are justifiable, why aren't they given a chance to participate? Why exclude them?

And in certain cases, certain private placements have a history of being shady (not saying that this is case with Notion).

A share placement sale or a private placement excludes and it prevents the minority shareholder the chance to participate EQUALLY.

Yes, if I were asked to vote, I would always VOTE AGAINST private placements. (I do hope you understand that this is my flawed personal preference, ok?)

- They need the money for the huge capex that they are going to incur this year for their capacity expansion....

The result for all these money spent u will see it in FY11 when their net profit will jump again due to more than 3x increase in their production capacity for HDD parts.

Now needless to say, since Notion claimed that all these money raised will be used for capex, surely one would imagine that the money spend should result in more net profit growth. That's the logical expectation and assumption. I have no problems with such reasoning.

However, let me stress that we are now looking at an increase of 29.270 million new shares, which works out to a 20.8% increase from the initial share base of 140.717 million.

And in my opinion, this is simply way too much in such a short time frame. January 2010, share base increase by 10%. Now Notion wants to increase by another 10%.

If one is a minority shareholder, what would one expect?

Which means, after these two share placements, Notion Vtec earnings has to increase by more than 20.8%, in order for the minority shareholders to see 'real growth' in their earnings per share.

Would this be possible?

Well those that really know me understand that I always feel that anything is possible.

So I let you be the judge and if you think the placement and the future prospects derived from the share placements is justifiable, do please buy more shares of Notion. :D

Who knows right? After all the plant expansions, Notions earnings could double or even triple, yes? That's a possibility yes?

But what if this does not happen? This is also a possibility, yes?

Me? Well I am only highlighting the issue of the dilution impact caused by these share placements. Whether the share goes up or down, it's beyond me. Really.

Honey, My Notion's Earnings Per Share Has Shrunk!

Notion reported it's earnings last night. On a q-q basis, it showed some weakness.

Here are some brief comments from the 'pros' on Notion recently.

The 'poor earnings' is expected said RHB Research!

- 2QFY10 results preview . Notion Vtec (NVB) will release its 2QFY10 results on 29 April. We estimate net earnings to fall marginally 5-7% qoq (vs. +9.2% qoq) to around RM13m due to: 1) seasonal factors; 2) strengthening of RM against the USD (+4.3% qoq); and 3) higher expenses stemming from the capacity ramp up in 2Q. This would bring 1HFY10 net profit to around 54-55% of our FY10 previous net profit forecast and around 53-54% of consensus estimates. However, we expect a strong qoq growth in 3Q-4Q10, driven mainly by: 1) higher volume loading of base plates from Samsung and strong contribution from higher margin spindle motor hub

However they still insist that it's a BUY.

- Investment case. We are maintaining our indicative fair value of RM4.59 based on a target PER of 10x FY 11 EPS. Hence, we reiterate an Outperform call on the stock.

On the Edge Financial Daily last week: Inter-Pac: Notion Vtec forging ahead

- We remain positive on Notion on the back of strong growth coming from both the HDD and SLR camera segments. Nevertheless, Notion is exposed to currency fluctuation as most of their HDD sales are carried out in the US dollar. The strengthening of the ringgit versus the US dollar will bite its bottom line slightly. Our fair value of RM3.78 is based on FY11 earnings per share (EPS) of 36 sen and PER of 10.5 times. — Inter-Pacific Research, April 20

KN in its most recent notes:

- Maintain forecast with unchanged target price of RM3.60 based on 11x CY2010F. Outlook for HDD remained robust with HDD majors including Seagate and Western Digital continuing to guide positively for the June quarter. BUY.

OSK had a trading buy call on 28th April ( err... target price is 3.38, Notion was trading at 3.26. - seriously wonder how on earth they can call it a buy with the target price a mere 12 sen or a mere 4% upside. But then.. what can I expect.. it's OSK! LOL!)

- Maintain Trading Buy and earnings forecasts. In the meantime, we do not expect Notion

to lose the other two antidiscs programs. The affected antidiscs program should have minimal impact on its FY10 and FY11 earnings.

However, this is not what I want to talk about.

Here is a snapshot of Notion's earnings. It's IMPRESSIVE.

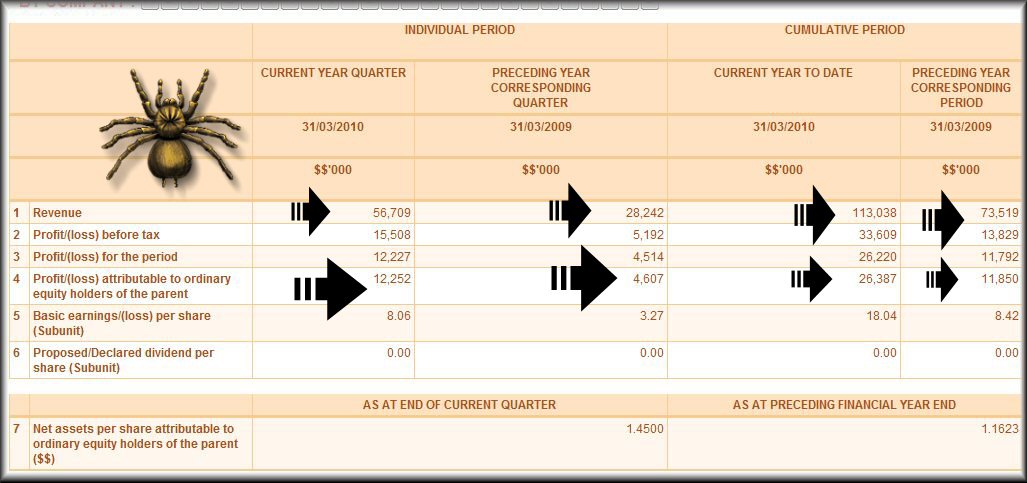

Sales is now on a different level and the jump in net profit can be clearly seen.

It's a wonderful set of results.

However... there's an issue.

Here's Notion's previous quarterly earnings: Quarterly rpt on consolidated results for the financial period ended 31/12/2009

Net earnings was 14.185 million. This quarter is only 12.252 million. Ah..yes the weakness in earnings as suggested by RHB.

Yes but this is NOT my issue.

Let's have a look at the earnings per share.

Now if one open the earnings notes on Notion's previous earnings, ( here is the link to the pdf file ), and look at page 8, one would see that Notion has stated it's earnings was based on 140.717 million. So from an earnings of 14.185 million, Notion's earnings per share is some 10.1 sen.

Notion's earnings reported last night was 12.252 million. Now if based on 140.717 million, Notion's earning per share should be some 8.7 sen.

But if you look at the screen shot, Notion's earnings per share stated was only 8.06 sen. An error?

No it was not. In yesterday earnings notes, Notion's earnings per share is based on 151.946 million.

And if I open my live quotes, here is what I am looking at.

Notion share base is now some 154.561 million.

Increased yet again.

Last night, beside reported its earnings, Notion announced the following:

- On behalf of the Board of Directors of NVB, Hong Leong Investment Bank Berhad wishes to announce that the Company proposes to undertake the following:

(a) Proposed issue of new ordinary shares of RM0.50 each in NVB (“NVB Shares”) not exceeding 10% of the issued and paid-up share capital of the Company through a private placement exercise;

(b) Proposed issue of up to 34,003,503 free warrants in NVB (“Free Warrants”) on the basis of 1 Free Warrant for every 5 NVB Shares held by the shareholders of the Company; and

More placements (Actually this is an OLD issue. See this OLD blog posting Notion Special Issues of Shares ) but this placement is sweetened by 'free warrants'.

Now if I open the pdf file attached, this is what I am looking at.

So before the warrants are given free... Notion's share base is to be enlarged to some 169.987 million.

Let's look at the impact.

From the earnings snap shot, we see Notion's earnings for 2 quarters was some 26.387 million.

Based on last quarters number of shares of 140.717 million, Notion's eps would equate to some 18.8 sen.

However, if based on this enlarged share base of 169.987 million, Notion's eps would be only 15.5 sen.

Now keeping it simple, let's assume that this was Notion's total fiscal earnings and that the market assigns a fair value earnings multiple of 12x to the stock. Yeah, a PE of 12. (Ass-u-me only, ok?)

Now based on an eps of 18.8 sen, Notion's fair value should be 12x18.8 ~ 2.26.

Now based on an eps of 15.5 sen, Notion's fair value should be 12x15.5 ~ 1.86.

See the difference?

The earnings per share has shrunk and so has the assumed target price!

How?

Do you like such share 'placements'?

And can you see how these share placements dilute your earnings?

Here's Notion's charts..

Thursday, April 29, 2010

The Pain In Spain

- Standard & Poor's cut its ratings on Spain by one notch to AA from AA-plus Wednesday, saying a longer-than-expected period of low growth could undermine efforts to cut the budget deficit.

The outlook is negative, reflecting the possibility of another downgrade if Spain's fiscal position worsens more than S&P currently expects, the agency said in a statement.

"In our opinion, Spain is likely to have an extended period of subdued economic growth, which weakens its budgetary position," Standard & Poor's said.

"We now project that real GDP growth will average 0.7 percent annually in 2010-2016, versus our previous expectations of above 1 percent annually over this period," S&P said.

That was from the article posted on CNBC: S&P Cuts Spain's Rating One Notch on Economic View

Despite the downgrade, on the Syndey Morning Herald Spain 'on track' after credit downgrade

- Spain is on track to bring its public deficit within an EU limit by 2013, its finance minister said on Wednesday after ratings agency Standard & Poor's cut the country's credit rating.

"We have a plan to reduce the deficit, we are putting it in place, we are meeting one by one all the timelines which we have set," Elena Salgado said during an interview with public television TVE.

"I believe the markets will evaluate the situation this way. When the situation in Greece is resolved, I believe things will return to their right place," she added....

Published on ABC.es. Un desliz del INE desvela que la tasa de paro superó en marzo el 20%, la peor desde 1997

With the help of Uncle Google's language translation: here

- An error by the National Institute Estadísitca (INE) provided further insights on the morning of yesterday, for a few minutes, unemployment data from the Labour Force Survey (LFS) for the first quarter of 2010 to be made public on Friday.

According to those who had access to the paper, the unemployment rate in the first quarter rose to 20.05%. Es It is the first time since 1997 that exceeds the benchmark rate of 20%. The clarification came in the early hours of the morning.

The EPA in the first quarter of 2010 indicates that the number of unemployed persons was 4.6127 million, ie more than 286 200 end of 2009 (4.3265 million). .....

A 20.05% unemployment?!!!

Surprisingly, this incredible high rate of unemployment is not unexpected. I remembered the following posting on Nakedcapitalism back in July 2009: Spain: Bleak forecast puts unemployment at 22% in 2010

- Citigroup has just released a forecast which is very troubling in regards to employment and growth in the Spanish economy. With unemployment already having hit 17.9%, Citigroup expects layoffs to increase this to 22% in 2010....

- Basically, things are looking bleak in Spain despite the positive spin some are putting on today’s numbers. Hopefully my last two posts on Spain, House price declines accelerate in Spain and Hypo Real Estate need for 10 billion also reveals huge problems in Spain, give you a sense that there is more downside to come for Spain’s property sector and its banking sector. This very definitely will negatively impact the employment market in Spain. Zapatero should feel lucky he was re-elected last year or he too would soon find himself unemployed.

Just published on Wall Straits Journal In Spain, Crisis Stays Low-Key

- By JONATHAN HOUSE

MADRID—Spain's worsening financial crisis remains a strangely low-key affair. One in five people here are out of work, but generous unemployment benefits, strong family support networks and a bustling informal economy are helping maintain people's lifestyles. Bars and restaurants in the city center are doing brisk business.

"It seems to me the situation here is less bad than in Greece," says Manuel Herrera, a 30-year-old Peruvian immigrant, who has seen the recent images of angry mobs protesting in Athens. "Here in Spain, the crisis is not so noticeable: People still go out for beers, to buy cigarettes, whatever."

But the Asian-restaurant chain he works for as a cook has closed down four of its 12 restaurants, and Mr. Herrera says he sees a sense of hopelessness setting in that could point to prolonged economic stagnation.

"The Spanish were not ready for this crisis," he says. "The situation's not getting any worse, but it's not getting any better either."

For years, Spain was one of the euro zone's biggest success stories. Membership in the common currency in 1999 brought historically low interest rates that fueled a credit and construction boom, which transformed the country into one of Europe's chief growth engines. Through 2007, Spain created more than one-third of all euro-zone jobs and absorbed four million immigrants.

The global financial crisis brought that crashing down. Spain is grappling with 20% unemployment and a double-digit budget deficit that threatens to land the country in a Greek-style financial crisis.

Though the government expects the economy to return to growth in the first quarter, that follows contractions in six consecutive quarters.

On Wednesday, Standard & Poor's cited low growth prospects resulting from mounting banking-system stress, high household debt levels and low export capacity as primary factors behind its decision to downgrade Spain's sovereign debt.

Thirty-year-old Eduardo lost his job as a computer programmer a year ago and says many of his friends are also out of work. He still isn't ready to take just any job: "There are jobs out there, but most of them don't pay to well, or they require higher levels of experience."

Until recently, the government of Socialist Prime Minister José Luis Rodríguez Zapatero has focused on anticrisis measures to cushion the pain of the unemployed by extending benefits, cutting taxes and taking measures to create short-term jobs for construction workers. It has gone to great pains to maintain good relations with unions.

But the government has changed gears amid mounting pressure from international investors to show it can pull the economy out of the doldrums and get its debt levels back on a sustainable path. It has announced plans to cut the public-sector wage bill, push back the retirement age and reform Spain's rigid labor market. The plans are vague thus far and have yet to ruffle many feathers.

The government is counting on a quick agreement on a support package for Greece to contain the euro-zone financial crisis and buy Spain more time to get its fiscal house in order. In an interview, Deputy Finance Minister José Manuel Campa said Spanish bond spreads have been blown out to "exceptional" levels that he believes are temporary. "Considering that they have been affected by the Greek situation, the sooner it is resolved, the better," he said.

Worth reading: No Wonder the Eurozone is Imploding

Could Greek Financial Crisis Hit UK Hard?

Could this be it? Greek financial crisis could hit Britain, warn economists

I was more interested in the last few passages...

- .... Delegates to the Institute of Directors' annual convention in London today said that they were concerned about the problems afflicting Greece spreading to the UK.

John McKenna, a director bakery ingredients business AB Mauri, said: “Hedge funds and currency speculators will just pick them off. When they have broken Greece they will move on to others, like they did with the banks.”

"The investors will go from Greece, to Portugal, Ireland, Spain and then will move to the UK. They will move to where they perceive the weakness to be.

“It is very similar to what has been happening to the banks. It is the first real test for the eurozone. If we let Greece go, then what is next?"

Paul Clark, director of the Potential Organisation, said: “The worry is what is following close behind [Greece]. It might be Portugal, that is just next door, and then Ireland. It all feels like it is coming much closer more quickly.

“It would be great to have some clarity on Europe about how much they want to do. Saying ‘thank God we are not in the euro’ does not quite cut it.”

Clare Richards, managing director for React Europe, said: “We are watching the situation very carefully. Of course it could spread and I am concerned.”

Martin Sorrell, the chief executive of WPP, one of the world’s biggest advertisers, told the conference: “We need the next Government to be on a war footing. A lot of people are thinking that is the economic challenge we face.”

George Osborne, the shadow Chancellor, also told the conference: "We should be concerned about what is happening in Greece and what is threatening to happen in Portugal. This is an illustration of the challenge we face.

“Thank God we are not in the euro. If we had been our boom would have been bigger and our bust would have been deeper and we would have been bailing out Greece."

Earlier a senior economist had warned of the risk of the spread of the problems from Greece to the UK.

Neil Mackinnon, from VTB Capital, told BBC Radio Four’s Today programme: “There are other countries that are fiscally challenged, if you want to use that phrase, very high budget deficit, very high debt GDP levels I’m thinking about Spain, Ireland, Italy and of course ourselves.

"We have a budget deficit as a per cent of our economy that is not to different from Greece, so the situation is spreading.”

He added that it was a “mystery” to him “why Britain has a triple A credit rating: "We have got a budget deficit that’s 12 per centof GDP our debt is doubling.

“It is escalating and I think the financial markets have already taken things into their own hands they are actually pricing in a downgrading of our credit rating anyway. ”

And Uk Media is already addressing this issue: Debt crisis: UK banks sitting on £100bn exposure to Greece, Spain and Portugal

- As analysts estimated that Britain's banks have a combined exposure of £100bn to Greece, Portugal and Spain – the three countries causing most concern on the financial markets – the Financial Services Authority was closely watching the markets and assessing exposures to the vulnerable countries.

After the ratings agency Standard & Poor's had downgraded Greek debt to "junk" yesterday, bank shares were knocked today but spared further falls as the downgrade of Spain's crucial credit rating came just as the stock market was closing. With UK banks standing to lose more in Spain than in Greece and Portugal, analysts said there might have been a more severe reaction if London had remained open longer today.

Analysts at Credit Suisse calculated that UK banks had £25bn of exposure to Greece and Portugal but £75bn to Spain, where the collapse in the property market has already forced banks such as Barclays to admit to bad debt problems and left Royal Bank of Scotland facing questions about its exposure.

"Lloyds' exposure to the three regions is likely to be negligible, we estimate that Barclays has £40bn exposure (predominantly loans in Spain and Portugal, excluding daily positions in Barclays Capital), and RBS has around £30bn–£35bn (again predominantly Spain, although we estimate £3bn to £4bn in Portugal and Greece as well)," the Credit Suisse analysts said.

Money markets, in which major banks lend to each other, also reflected the tension caused by the Greek downgrade with eurozone interbank lending rates enduring their biggest rise in nearly a year.

Much of the anxiety was targeted at French, German and Swiss banks. Howard Wheeldon, of BGC Partners, said: "If Greece defaults that means the pressure will then be felt and exerted on national banks that hold the Greek debt. That includes very many German, French and Swiss banks and it just may be that with so many banks involved one of these might just go down."

At today's annual meeting, RBS's chairman, Sir Philip Hampton, played down any exposure to Greece, while Lloyds' finance director, Tim Tookey, said on Tuesday that the bank had no "material [significant] exposure". Barclays publishes a trading update on Friday and will face questions about its exposure to the countries being downgraded.

In early trading today banks were the biggest fallers, with RBS tumbling 7%, Lloyds down by 6.5% and Barclays off 4%, though they recovered much of their losses by the time market closed.

Among continental European banks, analysts at Evolution calculated that Fortis, Dexia, CASA and Société Générale were most affected because of the value of their Greek debt holdings relative to their size.

According to Barclays Capital, UK banks account for only 3% of the exposure to Greek bonds, while data from the Bank for International Settlements shows that, at the end of 2009, Greece owed about $240bn (£160bn) overseas. Of this, France and Germany have the biggest exposures of $75bn and $45bn respectively.

Analysts expressed concern about the problems spreading. Daragh Quinn, banks analyst at Nomura, said: "Given the scale of the debt problem facing Greece, the prospect of some kind of debt rescheduling or even default are being considered as possibilities by the market. Sovereign risk concerns are also spreading to Portugal and Spain."

Only last week the International Monetary Fund, which has been called in to help fund the Greece deficit, warned about the impact of a sovereign risk crisis. "Concerns about sovereign risks could undermine stability gains and take the credit crisis into a new phase, as nations begin to reach the limits of public-sector support for the financial system and the real economy," the IMF said.

Credit Suisse analysts pointed out that not all the problems facing the markets were negative for the banking sector. "The increase in volatility should assist revenues at the investment banks, particularly for primary dealers like Barclays," the Credit Suisse analysts said.

"But there are clearly a number of important potential negatives. These include the potential for increased capital and liquidity trapping in affected sovereigns, or increased micro prudential requirements for local subsidiaries. Our bigger concern, however, is increased nervousness towards the UK," they added.

Greek debt crisis reaction: 'This could be bigger than anyone thought'

- "The mood in here is not quite as bad as it was after Lehman Brothers went under, but that's hardly a reason to celebrate," said one City bond trader. "But there's the same sense of not knowing how bad the contagion might get: sterling's taking a battering, bond spreads are widening dramatically, gold's flying again as investors flock to safe havens and bank lending across the EU is constricting, raising fears of another credit crunch."

.....I would say this is organised chaos," said Michael Hewson, a market analyst at CMC Markets. "The problem the eurozone has at the moment is the market does not believe anyone has any concrete plan in place to deal with the problem of Greece. What that is causing is some rather shredded nerves among bond holders."

According to David Jones, chief market strategist at IG Index, it feels like the early days of the credit crunch when Northern Rock went bust: "[It's] like when the run on the British banks started. Initially when the Greek crisis came to the fore, the thinking was 'maybe it's an isolated problem', but with the downgrade on Tuesday and now concerns about Italy, Ireland and Portugal, the worry is that it is going to be much bigger than anybody thought."

On BBC News: Could the UK face the same problems as Greece?

- So why, when both economies clearly have severe financial difficulties - has the UK managed to hang on to its much-coveted Triple A credit rating?

Here's the chart posted on that BBC News article:

The BBC article continues...

- "Clearly on the face of it we have a very similar deficit," says BBC economics editor, Stephanie Flanders. "However there are many things that are very different."

Market need

An obvious point is that Greece is still in recession with little sign of immediate improvements (its GDP is forecast to shrink by 3.5% in 2010).

The UK economy saw a return to growth in last three months of 2009 with initial figures showing this continued between January and March. The economy is forecast to continue to grow, albeit slowly.

Also, the UK's debt level, while high at more than 60% of GDP, is much lower than Greece's, which sits at about 115%.

And the type of debt is seen as significant too - with much of the UK debt not due for repayment for several years, unlike some other countries. It is predominantly made up of recently racked-up loans.

This means that it does not have to keep coming to the money markets to roll over the debt - in other words to refinance it.

"That's Greece's problem and other countries' too," our economics editor says. "They have to keep going to the markets. We're actually in a very strong position on that."

The UK's proven track record of increasing taxes and raising the money it says it is going to raise has also played in its favour, says Jeremy Batstone-Carr, research analyst at Charles Stanley.

"There are reasons to be concerned about Britain's need to tackle its deficit but we have not yet reached a critical point," he says.

"Credit rating agencies so far have given Britain the benefit of the doubt that we will enact the measures needed to bring down the deficit, however painful that will be."

'Line in sand'

Another advantage the UK has is that it controls its own currency - and so has a floating exchange rate.

Continue reading the main story Greece crisis: Is there an exit? Q&A: Greece's economic woes "It could, if it wanted to, devalue its currency, and that would relieve some of the pressure," says Mr Batstone-Carr. While such an action can have negative consequences as well as benefits - it is at least an option.

Greece, which entered the eurozone in 2001, does not have the luxury to act independently

On The Daily Mail Hung vote 'could tilt Britain into Greek financial turmoil'

- A hung parliament could lead to a Greek-style financial crisis, business leaders and economists said yesterday.

They warned of a run on the pound and loss of faith in Britain’s ability to tackle its deficit, which is on a par with that of Greece.

..... Miles Templeman, the institute’s director-general, said: ‘While political parties agree the deficit is a problem, there is little agreement on how it should be tackled.

'So it doesn’t surprise me that so many business leaders are worried about a hung parliament.

How?

The GBP vs the USD the last five days.

Would you be nervous about Britain becoming United King Down?

Wednesday, April 28, 2010

I Just Like KNM So So So Much

Hey it's not over.

Did I not say Why I Also Like KNM A Whole Lot and Why I Like KNM Even So Much More Today!

So many days after the failed KNM's MBO, finally there is Change in Boardroom!!

The MD has resigned...... great news eh?

But... but.... the MD who tried to do the ludicrous MBO is now given a new designation.

He is no longer the MD but the Chairman & Managing Director!!!!!!!!!!!!

Hallelujah! Hallelujah! Hallelujah!

Celebrations times comeon!!!!!!!!!!

And to make everyone happy... KNM rewarded their shareholders with some share buybacks!

Notice of Shares Buy Back - Immediate Announcement

*************************

Friday morning - 29/4/2010 edit:

KNM is now only 51 sen. It was 62 sen when I wrote Why I Also Like KNM A Whole Lot

Here's a not too smart a question. If I buy now at 51 sen, what if the company is taken private or another MBO is made, say at 40 sen? or 45 sen? or 50 sen? or even 55 sen?

Would I look smart?

Looking smart very important, yes?

***************************

Life is beach ball!!!

Yo... ye Liverpudians.... are you guys going to bring beach balls to the game this weekend?

:D

What Do You Expect After Greece Is Declared Junk?

What do you expect after S&P downgraded Greece's credit ratings were slashed to junk? (What took them so long to make this downgrade?)

Here is snippet from S&P:

------------------

Overview

- We have updated our assessment of the political, economic, and budgetary challenges that the Greek government faces in its efforts to place Greece's public debt burden onto a sustained downward trajectory.

- We are lowering our ratings on Greece to 'BB+/B' from 'BBB+/A-2' and assigning a negative outlook.

- The negative outlook reflects the possibility of a further downgrade if the Greek government's ability to implement its fiscal and structural reform program materially weakens in our view, undermined by domestic political opposition at home or by even weaker economic conditions than we currently assume.

....

Rationale

The downgrade results from Standard & Poor's updated assessment of the political, economic, and budgetary challenges that the Greek government faces in its efforts to put the public debt burden onto a sustained downward trajectory. We believe that the government's policy options are narrowing because of Greece's weakening economic growth prospects, at a time when pressures for stronger fiscal adjustment measures are rising. Moreover, in our view, medium-term financing risks related to the government's high debt burden are growing, despite the government's already sizable fiscal consolidation plans. Our updated assumptions about Greece's economic and fiscal prospects lead us to conclude that the sovereign's creditworthiness is no longer compatible with an investment-grade rating.

As a result of Greece's rising commercial borrowing costs, the authorities have requested extraordinary support from the Eurozone and the International Monetary Fund (IMF). We anticipate further information in the coming weeks from EU members regarding the terms and duration of support for Greece. We believe that a multiyear European Economic & Monetary Union (EMU)/IMF support program is likely, which should, in our opinion, significantly ease Greece's near-term liquidity challenges. Nevertheless, in our view, pressures for more aggressive and wide-ranging fiscal retrenchment are growing, in part because of recent increases in market interest rates. In our revised projections, we forecast Greece's net general government debt-to-GDP ratio reaching 124% of GDP in 2010 and 131% of GDP in 2011.

We continue to believe that the size and scope of the Greek government's fiscal consolidation program, and the government's political will to implement it, are the main drivers of our sovereign ratings on Greece. Sustained success in this regard could, in time, be reflected in lower market interest rates on Greece's debt. Early indications show that the government is likely to meet its 2010 deficit target. The authorities are also moving ahead with their

structural reform agenda, adopting tax reform in April, while proposals on pension reform are expected in May.

Nevertheless, we believe that the dynamics of this confidence crisis have raised uncertainties about both the government's administrative capacity to implement reforms quickly and its political resolve to embrace a fiscal austerity program of many years' duration. Based on our updated assessment, we estimate that the adjustment needed in Greece's primary fiscal balance relative to that of 2008 in order to stabilize the government debt burden amounts to at least 13% of GDP--a very high level compared with that which other sovereigns have been able to achieve. The government's resolve is likely, in our opinion, to be tested repeatedly by trade unions and other powerful domestic constituencies that will be adversely affected by the government's policies. At the same time, we expect official lender support to be highly conditional and revocable, and as such, we do not believe that it provides a floor under Greece's sovereign ratings.

As previously noted, the government's multiyear fiscal consolidation program is likely to be tightened further under the new EMU/IMF agreement. This, in our view, is likely to further depress Greece's medium-term economic growth prospects. Under our revised assumptions (see below), we expect real GDP to be nearly flat over 2009-2016, while the level of nominal GDP may not regain the 2008 level until 2017. Moreover, we find that Greece's fiscal challenges are increasing pressures on the banking and corporate sectors. In particular, we see continuing fiscal risks from contingent liabilities in the banking sector, which could in our view total at least 5%-6% of GDP in 2010-2011.

....

Outlook

The negative outlook reflects the possibility of a further downgrade if, in our view, the Greek government's ability to implement its fiscal and structural reform program is undermined by domestic political opposition or materially weakens for other reasons, including even weaker economic conditions than we currently assume.

We could revise the outlook to stable if we perceive that political support for government economic policies remains robust and Greece's economic growth prospects prove to be more benign than we currently anticipate.

---------------

On Bloomberg Businessweek: RBS Says Medium-Term Outlook for Euro Is ‘Extremely Challenging’

- April 27 (Bloomberg) -- The medium-term outlook for the euro remains “extremely challenging” because of risks the Greek debt crisis persists and extends to other countries in the region, according to Royal Bank of Scotland Group Plc.

Regardless of how Greece “is resolved in the short term, investors will remain underweight euro for the foreseeable future and a short-covering rally on a short-term resolution would be limited,” Greg Gibbs, a currency strategist in Sydney, wrote today in a report. The euro is “defying gravity,” which is “at odds with European sovereign debt markets,” he said.

On the UK Telegraph, Ambrose Evans-Pritchard reports: ECB may have to turn to 'nuclear option' to prevent Southern European debt collapse

- “We have gone past the point of no return,” said Jacques Cailloux, chief Europe economist at the Royal Bank of Scotland.“There is a complete loss of confidence. The bond markets are in disintegration and it is getting worse every day.

“The ECB has been side-lined in the Greek crisis so far but do you allow a bond crash in your region if you are the lender-of-last resort? They may have to act as contagion spreads to larger countries such as Italy. We started to see the first glimpse of that today.”

Mr Cailloux said the ECB should resort to its “nuclear option” of intervening directly in the markets to purchase government bonds.

This is prohibited in normal times under the EU Treaties but the bank can buy a wide range of assets under its “structural operations” mandate in times of systemic crisis, theoretically in unlimited quantities.

Mr Cailloux added: “This feels like the banking crisis in late 2008 post-Lehman, though it has not yet spread to other asset classes. The ECB will have to act it if does.”

Yields on 10-year Portuguese bonds spiked 48 basis points to 5.67pc, replicating the pattern seen as the Greek crisis started.

Portugal’s public debt will be just 84pc of GDP by the end of this year, far lower than that of Greece, at 124pc. However, its private debt is much higher and data from the IMF shows that its external debt position is worse.

Interest payments on foreign debt will be 8pc of GDP this year. Portugal’s net international investment position is minus 100pc of GDP, the worst in the eurozone.

The interest rate on a €9.5bn (£8.2bn) issue of Italian notes jumped to 0.814pc, up from 0.568pc in March. The bid-to-cover ratio was wafer-thin, falling to 1.02. Italy has the world’s third biggest debt in absolute terms.

The issue of the ECB buying bonds is a political minefield. Any such action would inevitably be viewed in Germany as a form of printing money to bail out Club Med debtors, and the start of a slippery slope towards in an “inflation union”.

But the ECB may no longer have any choice. There is a growing view that nothing short of a monetary blitz — or “shock and awe” on the bonds markets — can halt the spiral under way.

The markets are already looking beyond the €40bn to €45bn joint rescue for Greece by the IMF and the EU, questioning whether some form of debt restructuring or managed default can be avoided over the next year or two, or even whether the rescue plan can work at all in a country trapped in debt deflation with no way out through devaluation.

Professor Willem Buiter, a former member of Britain’s Monetary Policy Committee and now global economist for Citigroup, said there may need to be a “voluntary restructuring” of debt.

“It is quite likely that a haircut of, say, 20pc to 25pc will be imposed on creditors as parts of the deal,” he said.

The bond markets are already “pricing in” a default of some kind in Greece, where rates on 2-year debt spiked close to 15pc in panic trading yesterday. The European Commission and the International Monetary Fund both insist that restructuring is out of the question but investors have become cynical after months of EU rhetoric and foot-dragging by Berlin.

The ECB cannot lightly risk a second sovereign crisis erupting, with dangers of a spillover into Spain.

The exposure of Spanish-based banks to Portuguese debt exceeds $80bn, according to the Bank for International Settlements. There were early signs of strain in the Spanish banking system yesterday.

Banks were forced to pay a premium in the domestic “repo” market on fears of counterparty risk, although the Bank of Spain has so far won plaudits for ensuring that banks have large safety buffers.

It is unclear why the markets are becoming skittish over Italian bonds. Public debt is 115pc of GDP but this is offset by very low household debt.

Italian citizens are among the most frugal savers in the OECD club of rich states. Moreover, the government has weathered the financial crisis with a budget deficit in remarkable good health.

Portugal ratings were cut too.

- Portugal’s Rating

Portugal’s long-term local and foreign currency sovereign issuer credit ratings were cut yesterday to A- from A+ at S&P, which cited “fiscal and economic structural” weakness and also gave the nation’s debt a negative outlook.

“The downgrade was more aggressive than expected,” said Win Thin, a senior currency strategist at Brown Brothers Harriman & Co. in New York, referring to the reduction in Portugal’s debt rating. “If Portugal comes under attack, you get to Spain pretty quickly. ( source: here )

And of course with Greece debts no considered junk, I would ass-u-me that banks holding these Greek debts would soon need to replace those debt with capital.

And the markets tumbled. FTSE 100 suffers worst fall since November

How?

Have you check at the implications of last night events? Did you see what the charts are showing? Are you looking at the relevant charts?

Arrrghhhh... terrible way to start the morning eh?

Some light humour based on Goldman Sachs. (in case you need to ask, remember the movie 'A Few Good Men' starring Tom Cruise and Jack Nicholson?)

- "You want the truth? You can't handle the truth. Son, we live in a country with an investment gap. And that gap needs to be filled by men with money. Who's gonna do it? You? You, Middle Class Consumer? Goldman Sachs has a greater responsibility than you can possibly fathom. You weep for Lehman and you curse derivatives. You have that luxury. You have the luxury of not knowing what we know: that Lehman's death, while tragic, probably saved the financial system. And that Goldman's existence, while grotesque and incomprehensible to you, saves pension funds. You don't want the truth. Because deep down, in places you don't talk about at parties, you want us to fill that investment gap. You need us to fill that gap. "We use words like credit default swaps, collateralized debt obligation, and securitization? We use these words as the backbone of a life spent investing in something. You use 'em as a punchline. We have neither the time nor the inclination to explain ourselves to a commoner who rises and sleeps under the blanket of the very credit we provide, and then questions the manner in which we provide it! We'd rather you just said thank you and paid your taxes on time. Otherwise, we suggest you get an account and start trading. Either way, we don't give a damn what you think you're entitled to!" ( Source: here )

Tuesday, April 27, 2010

Them US Bankers Could Well Turn Into Real Estate Agents

Posted on WSJ's Real Time Economics : Number of the Week: 103 Months to Clear Housing Inventory

- 103: The number of months it would take to sell off all the foreclosed homes in banks’ possession, plus all the homes likely to end up there over the next couple years, at the current rate of sales.

How much should we worry about a new leg down in the housing market? If the number of foreclosed homes piling up at banks is any indication, there’s ample reason for concern.

As of March, banks had an inventory of about 1.1 million foreclosed homes, up 20% from a year earlier, according to estimates from LPS Applied Analytics. Another 4.8 million mortgage holders were at least 60 days behind on their payments or in the foreclosure process, meaning their homes were well on their way to the inventory pile. That “shadow inventory” was up 30% from a year earlier.

Based on the rate at which banks have been selling those foreclosed homes over the past few months, all that inventory, real and shadow, would take 103 months to unload. That’s nearly nine years. Of course, banks could pick up the pace of sales, but the added supply of distressed homes would weigh heavily on prices — and thus boost their losses.

The banks have 103 months to unload their housing inventory???

LOL!!!

It's only some 9 years plus. Only 9 years.

Aha!

But don't you worry about it since it's a capitalist world.

Let's see what can our beloved money loving bankers can do...

Create a property subsidiary, write down as much as possible the value of these housing inventory, sell them (how difficult is it to get good profit margins since the value written down low?), LIST THEIR SUBSIDIARY IN THE MARKETS, profit from the listing, Viola! No problem!

Say Doc, could them bankers have more houses to sell?

Pretty please... and if you don't mind, since our darling bankers are making more money, can they be paid more? Yeah, give them more compensation for all their hard work too!

Nothing wrong, yes?

And not forgetting this is such a non-issue. Doesn't anyone knows that them US Bankers don't make money via banking anymore? The bulk of the profit comes from their trading activities.

I wonder if them bankers should be reclassified as Trading Banks!

What a wonderful capitalist world this is.

Paul Krugman: Are The Rating Agencies Corrupted?

Posted the other day: Credit Ratings Sold For A Buck Or Two..

Paul Krugman had an editorial piece on NY Times: Berating the Raters

Some highlights from his piece.

- ... The bad news is that most of the headlines were about the wrong e-mails. When Goldman Sachs employees bragged about the money they had made by shorting the housing market, it was ugly, but that didn’t amount to wrongdoing.

Now get this..

- the e-mail messages you should be focusing on are the ones from employees at the credit rating agencies, which bestowed AAA ratings on hundreds of billions of dollars’ worth of dubious assets, nearly all of which have since turned out to be toxic waste. And no, that’s not hyperbole: of AAA-rated subprime-mortgage-backed securities issued in 2006, 93 percent — 93 percent! — have now been downgraded to junk status.

Bottom line? The rating agencies got it wrong by a whopping 93%!!!

Gosh, surely you would ask if them agencies knew what they were doing or are they simply incompetent?

If not... are they ....

- What those e-mails reveal is a deeply corrupt system. And it’s a system that financial reform, as currently proposed, wouldn’t fix.

Paul Krugman is calling it a deeply corrupt system.

"How can it be? It's simply capitalism at work here!!!"

Would you accept the above statement? This is all the work of a capitalist financial world?

- And it did. The Senate subcommittee has focused its investigations on the two biggest credit rating agencies, Moody’s and Standard & Poor’s; what it has found confirms our worst suspicions. In one e-mail message, an S.& P. employee explains that a meeting is necessary to “discuss adjusting criteria” for assessing housing-backed securities “because of the ongoing threat of losing deals.” Another message complains of having to use resources “to massage the sub-prime and alt-A numbers to preserve market share.” Clearly, the rating agencies skewed their assessments to please their clients.

Friday, April 23, 2010

Credit Ratings Sold For A Buck Or Two..

The buck or two is such an understatement.

Posted on Calculated Risk

From Kevin G. Hall and Chris Adams at McClatchy Newspapers: Senate panel: Ratings agencies rolled over for Wall Street

- A Senate panel investigating the causes of the nation's financial crisis on Thursday unveiled evidence that credit-ratings agencies knowingly gave inflated ratings to complex deals backed by shaky U.S. mortgages because of the fees they earned for giving such investment-grade ratings.

Thursday, April 22, 2010

Why I Like KNM Even So Much More Today!

But... but... but.... but....... the lower the stock falls, the better for the MD.

Which means he could come back with a new LOWER MBO offer price.

What a brilliant idea! The board of directors are not kicking him out, so why not make the stock fall lower and then offer a LOWER MBO price? Lower means cheaper. Good eh?

End of the day it's a rich man's world!

Which means if we are the smartest we could all jump in we could also make a nice tidy profit from his new LOWER MBO offer price!

How could we fail with such a sure win strategy?

After all, we do not know what the final offer price BlueFire Capital, together with GS Capital Partners and Mettiz Capital offered. ( Mettiz Capital is owned by Michael Tang Vee Mun, while GS Capital Partners is a unit of Goldman Sachs. (Goldman who???))

So smart KNM did not reveal what the final offer price was.

And because no price was revealed, the 90 sen price is already out-dated and out of the equation!

MIB (no it does not stand for Men In Black but it stands for Mayban Investment Bank) had believed ( or is it speculated?) that a final bid was made between 60 and 70 sen.

Objectivity is to get the offer price lower yes?

No money, no honey yes?

Now that KNM had dropped to just 60.5 sen, surely BlueFire Capital can squeeze the board of directors with an offer of 70 sen.

(Hmm.. at 90 sen, KNM is valued at 3.6 billion. at 70 sen KNM is valued at 2.8 billion. Wah! Cheaper by 800 million! Yeah every 10 sen down, KNM is valued 400 million cheaper. )

Yeah.. yeah... yeah... take it or leave it. (Life is good, no?)

So if we smarter, can we not jump in and whack the stock? how can we not win money?

Or if we are even the smartest, we wait for 50 sen.

If no offer come, we buy more at 40 sen.

Still no offer, we buy even more at 30 sen.

What 30 sen also no offer, sure win and no lose teeth la, we buy even much more at 20 sen.

Can ah?

How?

Life is good or life is simply GOOD!

Oh... I do need to make a disclaimer here.

Hmm.... Can I can guarantee that you may not make money if you simply follow my insane logic here? Can I use such disclaimer? Do I need such disclaimer?

On a less serious note, would it not be NICE (some use the word TRANSPARENT) that KNM comes clean and tell the public what was the final offer made by BlueFire Capital?

These F@#king Guys - Goldman Sachs

| The Daily Show With Jon Stewart | Mon - Thurs 11p / 10c | |||

| These F@#king Guys - Goldman Sachs | ||||

| ||||

Wednesday, April 21, 2010

Regarding Susccess Transformer Once More

I noted that I have been getting constant hits and referrals to the posting Comments On Success Transformer.

I believe I really should clarify more.

First thing first. I am seriously not a financial advisor and I really do not know if a stock will go up or down. Meaning to say, I really cannot guarantee if you could lose money if you follow what I post on this blog.

OK?

Secondly, that posting, Comments On Success Transformer, is NOT a recommendation. I was merely replying to a request made by blogger MaxWealth88.

Anyway, my points once more...

1. Success Transformer, had indeed done fantastic since listing but one needs to point out that the last three fiscal year, Success Transformer's earnings has gone up another level, thanks to its subsidiary, SEB.

2. now the subsidiary is to be listed. Do I like listing of a subsidiary? NO. Why? A company can easily list and delist its subsidiary. Risk is (a) you do not if it will happen (b) you do not know when it will happen (c) and if it does happen, you do not know if the privatisation price is fair or not. From a long term investing perspective, I believe this is not fair that such an option exist. (Yeah, need I be reminded that in a capitalist world, nothing is fair?)

That's my opinion why I don't like listing of a subsidiary. Of course, it's my personal dislike. You do not have to follow what I like or don't like. More so, I could always be wrong! :D

3. Again from a speculative perspective, yes from a trader/speculator perspective...

- .... Naturally the hope is, once Success is listed, both Success and SEB could trade higher. That's the hope, that's the objective.

And I do think many believe there is justification in such a strategy.

Is it wrong? Well, who am I to judge and say that such speculation will not work? And to be honest, let me say again, I do not know. Yes, the market is not mine and I have no idea what the market will or will not do. So sorry again if I am to disappoint you.

Let me repeat again what I wrote back then.. if this is the sole reasoning you are buying this stock, perhaps you could be extremely hardworking by digging out information on recent listing of subsidiaries in the market.

Did such a strategy work out?

Ok?

Why I Also Like KNM A Whole Lot

Let me see.

Do I like KNM?

Do you like KNM?

1. March 17th 2009, Management buyout of KNM hinges on funds. KNM then was 39 sen.

- “We are very undervalued. The opportunity for privatisation is a good opportunity but it’s the source of funding. There is no offer on the table,” said managing director Lee Swee Eng.

2. Wednesday, 10 June 2009, the Edge Financial Daily publishes the following. KNM’s MD sells 63.65m shares

- According to a Bursa Malaysia filing on Monday, Lee sold a total of 63.65 million shares representing a 1.6% stake in KNM between June 1 and 4 at prices ranging from 97.5 sen to RM1.02 apiece.

Regarding KNM's MD Disposal Of Shares For A Cool RM64 Million. Bottom line? MD makes a cool 64 million.

3. Feb 2010. Proposed Acquisition of the Entire Business and Undertakings of the Company (the "Proposal")

- KNM Group Berhad (“KNM”) has on even date received from BlueFire Capital Group Ltd (“Bidco”), an entity controlled by Ir. Lee Swee Eng, the Group Managing Director and major shareholder of KNM, a proposal to acquire the entire business and undertakings of KNM (“the Proposal”). The proposed price is equivalent to RM0.90 per issued ordinary share of KNM.

Hmm... what can anyone conclude?

March 2009, MD said KNM undervalued at 39 sen. Wants to take it private if got funds.

June 2009, MD disposes a chunk of shares between 0.975 and 1.02. MD pockets a cool 64 million.

4 Feb 2010. KNM now 75 sen. MD wants to do a MBO at 90 sen. (LOL! If 90 sen was a good price, how come he was disposing his shares like plague in June 2009?)

15 April 2010. KNM's MBO Fails. Stock plunges!

20th April 2010. KNM is now 62 sen.

Ah.. that's the way and I like it. Yessirme this is why I like KNM.

Oh... and the MD despite the failed MBO is still the MD.

Nice!

I like Scholes a whole lot too.

Tuesday, April 20, 2010

What Wall Street Crisis Are We Even Talking About?

Here's an article published last week: Speculating Banks Still Rule -- Ten Ways Dems and Dodd Are Failing on Financial Reform

- As we wind up for another dramatic bipartisan squabble over all the crap Wall Street flung at us, things are getting back to normal – for the wealthy. The top 25 hedge fund managers made a record $25.3 billion dollars in 2009. And despite all those dramatic congressional hearings, average compensation of Wall Street bankers rose by 27 percent in 2009.

Top 25 hedge fund managers made a record of $25.3 Billion in 2009.

Average Wall Street bankers compensation rose by 27% in 2009.

Where's the Wall Street crisis?

What Wall Street crisis are we even talking about?

Life is freaking good, eh?

From the same article.

- On the other side of humanity, more sobering numbers include a record 2.8 million properties in foreclosure for 2009, a 21 percent increase over 2008's astonishingly high figure, with another 4.5 million foreclosures projected for 2010. Federal mortgage modification plans have not stemmed this tide, because lenders aren't required to particiapte; and lenders, in the words of Herman Melville's Bartleby, "would prefer not to" renegotiate a mortgage for which they'd then have to book a loss. As foreclosures continued to climb, so did bankruptcies, rising 35 percent in 2009 over 2008 levels.

More foreclosures. More bankruptcies.

Who cares about the poor? Screw the poor.

Make them bankers rich!

- "Banks -- shockingly -- aren't helping. They posted their lowest lending rates since 1942; despite all the subsidies and cheap money they received from, well, us, including exceedingly low Federal Reserve loan rates (zero to 0.25 percent interest)."

What a wonderful world this is!

Yeah, the banks are recording better numbers. What crisis?

But.. how many of these bankers are making the money the old fashion banking way? Does it bother anyone that the bulk of the money earned by the banks are made via extraordinary items such as accounting profits and yeah, them bankers apparently are now super duper traders too! Trading profits are so easy for them bankers.

But who cares, right?

We need the good news. We ONLY want the feel good financial news.

Does anyone even care how the trading profits are made?

News like Ex-Goldman trader blows whistle on silver and gold manipulation does not matter.

Yeah.. how cares?

Yeah.. most important them bankers make money!

Life is simply superb!

Subscribe to:

Posts (Atom)