Notion reported it's earnings last night. On a q-q basis, it showed some weakness.

Here are some brief comments from the 'pros' on Notion recently.

The 'poor earnings' is expected said RHB Research!

- 2QFY10 results preview . Notion Vtec (NVB) will release its 2QFY10 results on 29 April. We estimate net earnings to fall marginally 5-7% qoq (vs. +9.2% qoq) to around RM13m due to: 1) seasonal factors; 2) strengthening of RM against the USD (+4.3% qoq); and 3) higher expenses stemming from the capacity ramp up in 2Q. This would bring 1HFY10 net profit to around 54-55% of our FY10 previous net profit forecast and around 53-54% of consensus estimates. However, we expect a strong qoq growth in 3Q-4Q10, driven mainly by: 1) higher volume loading of base plates from Samsung and strong contribution from higher margin spindle motor hub

However they still insist that it's a BUY.

- Investment case. We are maintaining our indicative fair value of RM4.59 based on a target PER of 10x FY 11 EPS. Hence, we reiterate an Outperform call on the stock.

On the Edge Financial Daily last week: Inter-Pac: Notion Vtec forging ahead

- We remain positive on Notion on the back of strong growth coming from both the HDD and SLR camera segments. Nevertheless, Notion is exposed to currency fluctuation as most of their HDD sales are carried out in the US dollar. The strengthening of the ringgit versus the US dollar will bite its bottom line slightly. Our fair value of RM3.78 is based on FY11 earnings per share (EPS) of 36 sen and PER of 10.5 times. — Inter-Pacific Research, April 20

KN in its most recent notes:

- Maintain forecast with unchanged target price of RM3.60 based on 11x CY2010F. Outlook for HDD remained robust with HDD majors including Seagate and Western Digital continuing to guide positively for the June quarter. BUY.

OSK had a trading buy call on 28th April ( err... target price is 3.38, Notion was trading at 3.26. - seriously wonder how on earth they can call it a buy with the target price a mere 12 sen or a mere 4% upside. But then.. what can I expect.. it's OSK! LOL!)

- Maintain Trading Buy and earnings forecasts. In the meantime, we do not expect Notion

to lose the other two antidiscs programs. The affected antidiscs program should have minimal impact on its FY10 and FY11 earnings.

However, this is not what I want to talk about.

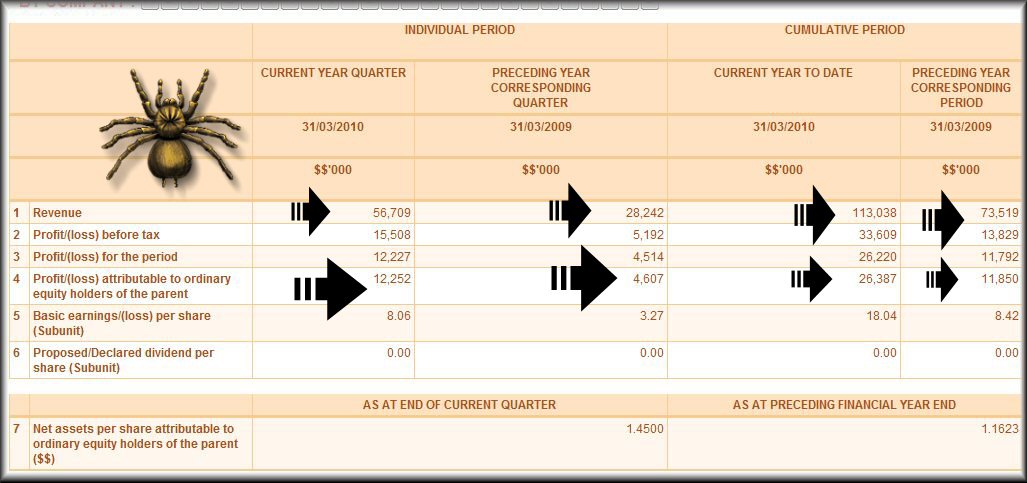

Here is a snapshot of Notion's earnings. It's IMPRESSIVE.

Sales is now on a different level and the jump in net profit can be clearly seen.

It's a wonderful set of results.

However... there's an issue.

Here's Notion's previous quarterly earnings: Quarterly rpt on consolidated results for the financial period ended 31/12/2009

Net earnings was 14.185 million. This quarter is only 12.252 million. Ah..yes the weakness in earnings as suggested by RHB.

Yes but this is NOT my issue.

Let's have a look at the earnings per share.

Now if one open the earnings notes on Notion's previous earnings, ( here is the link to the pdf file ), and look at page 8, one would see that Notion has stated it's earnings was based on 140.717 million. So from an earnings of 14.185 million, Notion's earnings per share is some 10.1 sen.

Notion's earnings reported last night was 12.252 million. Now if based on 140.717 million, Notion's earning per share should be some 8.7 sen.

But if you look at the screen shot, Notion's earnings per share stated was only 8.06 sen. An error?

No it was not. In yesterday earnings notes, Notion's earnings per share is based on 151.946 million.

And if I open my live quotes, here is what I am looking at.

Notion share base is now some 154.561 million.

Increased yet again.

Last night, beside reported its earnings, Notion announced the following:

- On behalf of the Board of Directors of NVB, Hong Leong Investment Bank Berhad wishes to announce that the Company proposes to undertake the following:

(a) Proposed issue of new ordinary shares of RM0.50 each in NVB (“NVB Shares”) not exceeding 10% of the issued and paid-up share capital of the Company through a private placement exercise;

(b) Proposed issue of up to 34,003,503 free warrants in NVB (“Free Warrants”) on the basis of 1 Free Warrant for every 5 NVB Shares held by the shareholders of the Company; and

More placements (Actually this is an OLD issue. See this OLD blog posting Notion Special Issues of Shares ) but this placement is sweetened by 'free warrants'.

Now if I open the pdf file attached, this is what I am looking at.

So before the warrants are given free... Notion's share base is to be enlarged to some 169.987 million.

Let's look at the impact.

From the earnings snap shot, we see Notion's earnings for 2 quarters was some 26.387 million.

Based on last quarters number of shares of 140.717 million, Notion's eps would equate to some 18.8 sen.

However, if based on this enlarged share base of 169.987 million, Notion's eps would be only 15.5 sen.

Now keeping it simple, let's assume that this was Notion's total fiscal earnings and that the market assigns a fair value earnings multiple of 12x to the stock. Yeah, a PE of 12. (Ass-u-me only, ok?)

Now based on an eps of 18.8 sen, Notion's fair value should be 12x18.8 ~ 2.26.

Now based on an eps of 15.5 sen, Notion's fair value should be 12x15.5 ~ 1.86.

See the difference?

The earnings per share has shrunk and so has the assumed target price!

How?

Do you like such share 'placements'?

And can you see how these share placements dilute your earnings?

Here's Notion's charts..

2 comments:

Hi there,

the EPS is definitely going to get diluted this year. But u need to understand what the private placement is for. They need the money for the huge capex that they are going to incur this year for their capacity expansion.

The result for all these money spent u will see it in FY11 when their net profit will jump again due to more than 3x increase in their production capacity for HDD parts.

An example of how brokers (and I didn't say OSK) screw us over:

It often happens that an insider goes to the head of a brokerage concern and says: "I wish you'd make a market in which to dispose of 50,000 shares of my stock."

The broker asks for further details. Let us say that the quoted price of that stock is 50. The insider tells him: "I will give you calls on 5000 shares at 45 and 5000 shares every point up for the entire fifty thousand shares. I also will give you a put on 50,000 shares at the market."

Now, this is pretty easy money for the broker, if he has a large following and of course this is precisely the kind of broker the insider seeks. A house with direct wires to branches and connections in various parts of the country can usually get a large following in a deal of that kind. Remember that in any event the broker is playing absolutely safe by reason of the put. If he can get his public to follow he will be able to dispose of his entire line at a big profit in addition to his regular commissions.

* taken from Reminiscences of a Stock Operator, Edwin Lefevre *

Post a Comment