Let me try something new.

I have blogged too many times on AirAsia's earnings. ( Refer postings here: AirAsia )

AirAsia reported its earnings tonight.

How now Brown Cow?

What do you think? Do you like what you see?

( haha.. this something new... a rather lazy new way, eh? :P )

---------------------

- bullbear said...

I like your posts when YOU provide the answers. I absolutely rank this post your worst so far. :-) Cheers. ;-)

Alamak! Worst post ever?

Are you sure?

Hehe... guess what? I do agree! :P (ps: I have no answers on how the moo moo cow jumped over the moon! )

- K C said...

“Never invest in anything that eats or needs painting.” Billy Rose

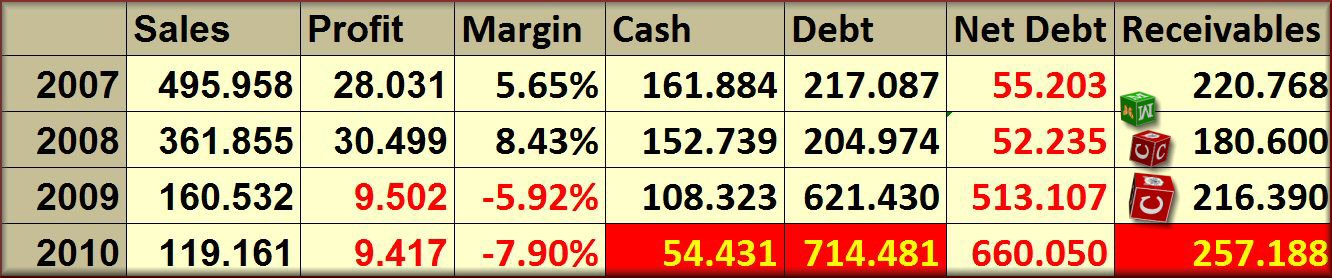

AirAsia made an EPS of 38 sen and with its share at 2.35, it is selling at a PER of only 6. It has 1.5 b in cash. Great?

No it sucks to the bone! It borrows 7.86 b! this leaves it with negative cash of 6.36 b! Are they required to pay the 720m deferred tax which is classified as an asset too? Cash flows from operations of 1.9b but how much has to plough back for capex? It has been negative free cash flow in terms of billions for the past years. Scary, isn't that? That is the peril of just looking at earnings.

Errr.... extremely valid points but....

I am not too motivated to talk about eps and per. Sorry.

However, as most would know, I am not a fan of AirAsia but.... sometimes I do have to give credit when credit was due.

Let's see, when AirAsia was listed, I did not like how they marketed their stock. It was all talk and most important issue to the investing public was 'did AirAsia live up to their IPO proforma promises?' My answer is a flat no.

The company made extremely optimistic forecasts during their IPO. They boldly told the investing public that it would triple its earnings within a year after listing and needless to say, some would argue that by having such optimistic earnings forecasts, the company would able to market their shares much higher. And AirAsia failed to deliver what it had promised during its IPO. ( Do refer to this old posting AirAsia. )

And then it made losses when they gambled with their hedging. Yes, I understand by using the word gamble, it's a rather big word but one can refer to this 2009 posting Regarding AirAsia Fuel Hedges Again where AirAsia mentioned in the local media 'No more bets on oil price'.

Yeah.

I was less than impressed.

And neither was I impressed with their bold buyout saga back in 2008. ( see Huh? AirAsia Buyout Still An Option????? - it failed because Tune Air Says Unable To Secure Financing !!! )

Anyway ... the extreme weakness in AirAsia balance sheet was well documented many times. So was the deferred tax issue and how AirAsia declared it to be an asset but what do I know since I am not an accountant and I never studied it before. :)

It was scary the size of AirAsia debts and the size of the capital commitment for new aircrafts. How on earth did AirAsia manage to make such a gutsy order for new aircrafts given the weakness in their balance sheet? It was unreal.

Things however did change.

Should one call it great business hindsight? Or should one call it pure luck?

First they managed to get the big boost when they managed to do a share sale and from that placement of shares, they managed to raise some 500 million in 2009. That was crucial in my flawed opinion.

And then... the USD weakened and the oil prices fell.

It was a double booster.

Their borrowings was predominantly denominated in USD. With the weaker USD, it meant they now owed less in RM and I do understand that some would say it's a silly reasoning because AirAsia still needs to pay it and who knows by the time they actually pay, the USD could rise. However, as it is, what matters to the financial markets is that at the moment, AirAsia now owes less.

Anyway my previous posting on AirAsia was A Look At AirAsia Stellar Earnings. In that posting I had updated AirAsia main financial numbers.

Compare that to yesterday earnings.

Earnings was actually flat. The previous year same quarter comparison is NOT meaningful in my opinion.

Cash actually improved a lot compared to the previous quarter.

And debt increased slightly.

But the capital commitment... there was a huge improvement, yes?

And as mentioned before in August 2010, I thought it was a Positive Move That AirAsia Defers Their AirBus Order.

Seriously... it's giving AirAsia a fighting chance to survive!!!

And I still hold those remarks from that posting.

- However, let me say this, I have to give AirAsia some credit for eating the humble pie and for successfully persuading AirBus to allow them to defer the delivery of the air crafts and more so, this move really gives them a fighting chance to survive and to overcome their insanity of building a company which was clearly over burdened by the immense corporate debts they took upon to finance the building of their business.

Yeah.. AirAsia should be ok for the next one year or so... yeah.. this is a POSITIVE CORPORATE exercise... it's certainly extremely crucial that AirAsia made this postponement of delivery.... but... deferring is only a postponement.... and in regardless, these air crafts order still needs to be delivered! - Anyway... a postponement is a postponement is a postponement. Come 2014 (last August AirAsia deferred 8 AirBus to 2014) and 2015, these air crafts still needs to be delivered. Which means, from now till then, AirAsia still needs to ensure that it builds up its cash flow to ensure it can accept delivery of these air crafts that they had ordered. Unless of course, AirAsia can pull off another miracle by asking AirBus to allow them to defer yet once more. :P

ps: yeah, AirAsia X listing would indeed help AirAsia financials. It too is required. And it is the ONLY OTHER logical and sensible option for AirAsia to rescue its dire balance sheet.

Back in early 2009, I certainly thought AirAsia was doomed. I really thought there was a 90% chance it go into deep trouble but now I have changed my opinion. It's doing all the right things to survive.

They got their placement of shares. They deferred their aricraft order and their current plans to list AirAsia Thailand would help a lot!

But then the main issue or risk is... 2014 and 2015.

That's when AirAsia would have to take deliveries of all the aircrafts orders they have postponed. Will they survive? Or will they not?

ps: I have no idea what the stock would do. :/

- tklaw said...

Hi Moolah,

Most investors would ignore dividend or debt level during bull runs.

What they care is profit level...Capex? too far to think of it. Making good profit will boost share price. short term profit is more important..haha

Hope you understand that this is NOT a posting suggesting AirAsia would go up or down.

You do undertstand that, don't you?

Quote: "Most investors would ignore dividend or debt level during bull runs." ..... err... most investors? I am sure some investors would strongly disagree about such a statement.

But what do I know? :=)