Maxtral was listed in Aug 2003 via a RTO of General Lumber and in the restructuring exercise it involved the exchange of 10 Lumber shares into1 maxtral share and also there were some ICULs involved. Back then some 149.9M ordinary shares and 144.6M ICPS were issued. At the moment of writing, Maxtral has some 210.099 million shares and it has some 84.415 million shares of ICUL outstanding. (ICP can converted on 1-1 basis)

And another worthwhile point is that Maxtral has a private placement exercise of 88.354 million shares. This exercise had been approved but for some reason or another, it has been delayed and in its latest announcement back in Aug 2006, this pp has been granted extension till March 2006.

Couple of things - PP always dilute earnings and this 88.354 pp represents a possible dilution of close to 30% - assuming full conversion of iculs. Secondly, why not laku? Perhaps a bad manager for this exercise? (PM Securities is handling Maxtral's PP woh). PP in a hot market, could sometimes do strange stuff to a stock woh - i guess Unker will know what i mean. But timber is now hot. Perhaps, Maxtral could find some buyers for this PP.

Anway, this is Maxtral background according to surff-fatt-fatt back in 2003.

Tawau-based manufacturer of plywood, veneer and moulding products. Tawau-based Maxtral commenced business in 1990. Its plywood and veneer capacity was last doubled to 8,000 cu m per month in 2002, while the monthly capacity for moulding products has remained at 1,500 cu m in the past five years. Based on the latest available information, Maxtral operates at about 70% of its plywood capacity, and less than 20% of veneer.

Multi-sourcing for log supply. Maxtral has a log supply agreement for 15,000 cu m per month from Aug 2002 to Jul 2005 (with option to extend to Jul 2008), which is sufficient for its current log requirements. In the past, Maxtral has sourced logs from Indonesia, Brazil and New Zealand to capitalize on supply and pricing opportunities, and expects to still do so in future. We understand that it also intends to acquire its own timber concession while developing alternative wood sources such as from oil palm tree trunks or forest plantations.

US the main export market. Maxtral derives about 70% of its revenue from the export market, of which about 30% goes to the US. This followed a switch from predominantly Japan previously. Maxtral has a fairly high customer concentration with its top five customers accounting for more than 50% of revenue.

Maxtral has a two-year contract (beginning Nov 2002) to supply between 2,000 cu m to 5,000 cu m of FSC certified (timber certification for quality and environment practices) products per month to a Hong Kong-based customer, and a one-year contract to sell up to 3,000 cu m of veneer per month to a Korean company. Taking the lower end of the first contract and assuming half the maximum commitment for the second, Maxtral would have secured about two-thirds of its actual output in 2002 through the two new contracts. As both only started in late-2002, Maxtral should look towards higher profitability in 2003.

Couple of things.. the log agreement thingy. the option to extend to 2008. If Maxtral exercised that option it should be recording some decent profits. However, on the other hand, one should realise that Maxtral, like a couple of other timber/plwood stocks, it does not own its own timber concession. Hence Maxtral needs to source for its timber.

That was then.

So what has Maxtral done since?

Sales Earnings

2003 36.918 3.830

2004 100.354 5.880

2005 158.247 11.502

ttm 194.724 14.810

ttm = trailing tweleve months or most recent 4 quarters.

The ttm is indicating that Maxral should have a really decent fy 2006. So far, Maxtral last reported earnings was on 30th Aug 2006 and it reported its first half (2 quarters) earnings for fy 2006 to be at 6.973 million (which is much more than what Maxtral did last year (3.551 million) (and histroically, Maxtral q3 and q4 earnings is much stronger). And with most timber stocks showing really decent earnings, Maxtral earnings should be strong.

Here is the snapshot of earnings.. (note how Q3 and Q4 earnings is always stronger)...

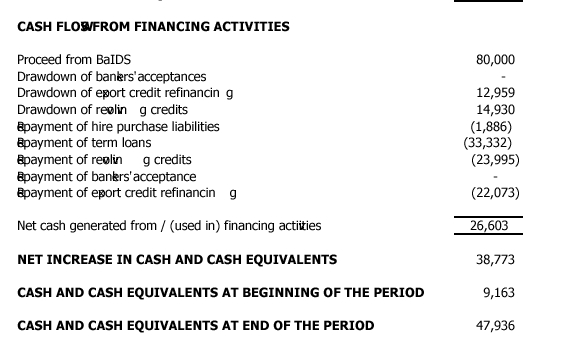

Here is Maxtral's Balance sheet and Cash Flow

Maxtral is covered by ... and this is a snippet of what they wrote back on 1st Sept 2006.

Friday, 1 September 2006

BUY Price RM0.280 Target RM0.330Mervin Chow Yan Hoong

Growing Up Well On Fertile Soil

Above expectation. Maxtral’s 1H06 turnover and net profit grew a massive 55.5% and 95.6% y-o-y respectively. Quarterly comparison, we saw a 60.3% and 25.9% YoY improvement in turnover and net profit as compared to 2Q05. Annualised net profit came in at RM13.5m, 43.8% above our forecasted figure.

Benefiting from high demand for timber products and shortage of logs. Growing up in an environment of shortage of logs which has led to increased demand for logs and other timber products, Maxtral is poised to gain and grow favourably since the recent run-up of prices for these products (Figure 3). Maxtral also has an exclusive access to 10,000 hectares of natural forest which will provide the Group with a steady large supply of logs for about 7 years. In addition to the benefit that Maxtral’s logs in the market will be able to fetch a very good price, availability of these in-house logs will also have significant and favourable impacts on the logs and timber products division’s earnings as its log input costs will be lower. In addition, we believe that the Group’s veneer and plywood division still has an excess capacity of about 40%-30%, which will also enable it to continue to meet the high and growing demand for these timber products.

Going for further expansion. The Group is issuing a RM100m Islamic Securities Facilities in which part of the proceeds will be utilised to finance the purchase of raw materials, capital expenditures and working capital of Maxtral. As part of the Group’s strive to upgrade its expertise, plant and machinery and range of products to meet the needs of its customers, Maxtral is investing RM15m to purchase a wood chip fuelled plant to mitigate the hike in diesel and upgrading of the mill infrastructure and facilities.

Venturing into oil palm industry. As part of the Group’s diversification strategy, Maxtral is planning to venture into the oil palm industry, which will give it positive contribution to top and bottom lines in the near future. However, things are still are not firmed yet as discussions are at their preliminary stage.Reiterating BUY at RM0.33 target price (Figure 5). At current share price, Maxtral could still offer a further potential upside of 19.5%. As the Group is still in need of large working capital to grow, Maxtral is yet to pay any dividends to-date. However, management has indicated that it could potentially establish a longer-term dividend policy soon.

Ok, so what we have?

The OSK report surprising reports that ..

Maxtral also has an exclusive access to 10,000 hectares of natural forest which will provide the Group with a steady large supply of logs for about 7 years. In addition to the benefit that Maxtral’s logs in the market will be able to fetch a very good price, availability of these in-house logs will also have significant and favourable impacts on the logs and timber products division’s earnings as its log input costs will be lower.

Interesting because surf-fatt-fatt said Maxtral has to source for its logs.

And another interesting issue is that MAxtral was at 28 sen when Osk wrote the report back on 1st Sept 2006.

Maxtral is now .. 0.40/0.405.

Maxtral share price has appreciated quite a bit and the next driver for the stock is how Maxtral perform in its q3, which would be released these few days.

Would it be a blow-out quarter as seen by most other timber stocks?

As it is, Maxtral's ttm profit is at 14.8 million, which equates to an eps of 7 sen (fully diluted eps - assuming full conversion of icul is at 5 sen).

yesterday, tekala, announced its earnings. For a rather lacking timber stock, tekala too had a blowout earnings. q-q earnings improved from 1.645 million to 4.035 million.

So perhaps.. i would have to agree with you that Maxtral earnings has a pretty decent chance to outperform as well.

rgds

2 comments:

wah this place really geng woh... so many treasures also

Y1

I bought this share at 36.5 sen and i believe this stock can offer more than my intrinsic value of 41.7 sen.

http://nik271.blogspot.com/2006/11/portfolio-update-17-november-2006-to.html

Post a Comment