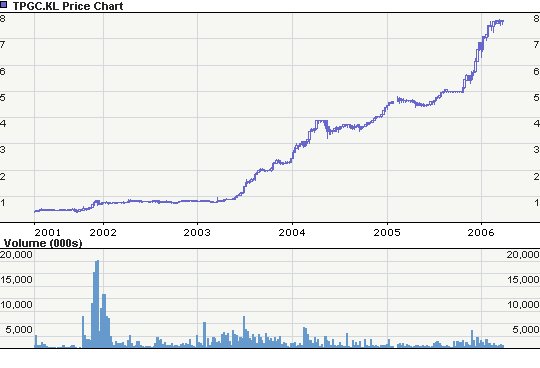

Back in 2001... that was the year Top Glove was listed on KLSE. On Oct 2001, they announced their 2001 q 4 earnings. (it would good to note the announced their very aggressive ambition, Top Glove Forecasts 40% Sales Growth two days after releasing their 2001 results)

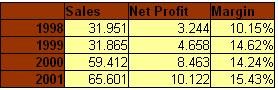

total sales. 138.662 million

net ytd profit. 17.217 million

Cash & equiv 9.824 million

total debts 13.958 million

Did it deliver? A year later on Oct 2002, they announced their 2002 q4 earnings.

total ytd sales. 181.055 million

total ytd net profit. 18.036 million

Cash & equiv 21.214 million

total debts 13.440 million (net cash 7.774 million)

Sales revenue increased a lot but profit were flat. Ahh.. cash grew nicely.

Under the title of Margin Pressure, dated 22 Oct 2002, Surf 88 wrote the following...

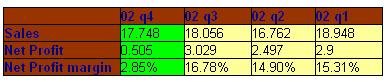

- Margin squeeze. In our previous result commentary (see ), we highlighted that Top Glove (RM2.12, stock code 7113) could have locked in rubber stocks at lower prices and hence the impact of higher rubber prices would only manifest in Jun-Aug 2002. This appears to be the case, as operating margin dropped to 13.9% in Jun-Aug 2002 from 16.0% in the preceding quarter. As such, pretax profit only rose 6% despite 19.0% turnover growth. Deferred taxation further depressed net profit to show an 11% decline.

Results in line. Overall, the full-year results were within our expectations, where topline growth was largely driven by a 23% capacity expansion but profits did not keep pace as margins fell from 17.3% to 14.9% due to higher raw material costs.

And here is a snippet from a Star interview back in 2002...

- According to Lim, Top Glove’s second factory in Thailand is scheduled to begin operation next month while the one in China will start in March next year. Top Glove currently also has five factories in Malaysia.

New 2nd factory starting in Thailand... the start... the begining of the explosive, promised growth in earnings.

Here is Top Glove's 2003 Q4 quarterly earnings.

total ytd sales. 265.089 million

total ytd net profit. 25.222 million (ahh... ze big jump in net earnings!!!)

Cash & equiv 22.051 million

total debts 39.289 million (net debt of 17.238 million)

point to note... last fiscal year, Top Glove was in a net cash position. To achieve the jump in net profit, from 18.063 million to 25.222 (or an an increase of 7.159 million), Top Glove went from a net cash position of 7.774 million to a net debt of 17.238 million.

So, a year later... the big jump in earnings happened and Top Glove delivered.... but alas.... Surf 88 sudah bungkus by then .... anyway we now see that this company has really, really been aggressive. Many new production lines were set-up, new plants... and most of all.... we have Ze birdie thingy!

Ahhh.... good birdie fortunes + aggressive expansion = fantastic growth for 2003.

Now, here is Top Glove's 2004 Q4 quarterly earnings.

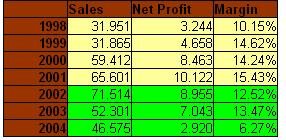

total ytd sales. 413.967 million

total ytd net profit. 39.509 million (wow.. bigger jump in net earnings!!!)

Cash & equiv 30.226 million

total debts 63.063 million (net debt of 32.837 million)

again some points to note... last fiscal year, Top Glove was in a net debt position of only 17.238 million. To achieve the 'additional growth', from 25.222 million to 39.509 (or an an increase of 14.287 million), Top Glove went from a net debt position of 17.238 million to a net debt of 32.837 million. (or it increased its net debt position by 15.599 million). How was their expansion justifiable?

anyway how was Top Glove achieving its super duper Top Glove? Here is some RHB notes which indicates that the growth is via acquisitions of new factories and starting of new production lines...

- It has commissioned two new lines each in Factory 5 in Ipoh and Factory 6 in Phuket at end-August 2004. In Factory 5, Ipoh, the target is to install 10 new lines, bringing its capacity to 175m pieces a month, from the current level of 110m pieces a month. In Factory 6, Phuket, the plan is to replace the existing seven production lines with 10 advanced production lines, lifting capacity from current level of 35m pieces a month, to 65m pieces a month. Meanwhile, installation of new lines in Factory 10 is in progress while construction of Factory 11, Klang is going on full steam. It aims to commission a total of at least 155 production lines with annual capacity of 13.0bn pieces a year by end-2005. It has identified two new sites for two new factories which will be constructed in CY2005 and CY2006, respectively.

It has completed the acquisition of the remaining 40%-stake in Factory 7 in Hatyai, Thailand on 11 October 2004. Plan is in place to increase its capacity from current level of 1.08bn pieces a year to 4.8bn pieces a year by end-FY06. Its proposed acquisition of the remaining 45%-stake in the China plant is expected to complete by end-1QFY05.

How?

ok ... let me try to give an unbiased view on what is happening... :D.... try hor...

Firstly when there is huge spikes in sales & net profit, the first thing i always check on is whether there was any company acquisition which might have caused the spike in earnings.

Well, what i saw is TG is simply a very aggressive and ambitious company. It started off by buying a couple of factories in Malaysia and started expanding its production lines. It then moved on to Thailand and it even moved into CHina.

So over the years, TG focus was simple. Aggressive growth thru acquisitions and organic growth. And plans to stick to this gameplan for the next few years.

And of course all this has been helped by the birdie issue in 2003.

And the end result, although we are seeing the fantastic growth in earnings, TG is paying a hefty price for their expansion.

And last year, Oct 2005, Top Glove reported its 2005 Q5 quarterly earnings.

total ytd sales. 641.827 million

total ytd net profit. 58.141 million (wow.. earnings still very good!!!)

Cash & equiv 31.755 million

total debts 154.191 million (net debt of 122.436 million!!)

How?

Let's look at those issue or rather those points again.... last fiscal year, Top Glove was in a net debt position of 32.837 million. To achieve the 'additional growth', from 39.509 million to 58.141 million (or an an increase of 18.632 million), Top Glove went from a net debt position of 32.837 million to a net debt of 122.436 million. (or it increased its net debt position by 89.599 million).

How was their expansion justifiable?

Which was why I blogged that posting in Oct 2005. And let me repeat the main issues.

Sooooooooooo despite it’s great sales and net profit growth… it’s bottom-line certainly ain’t too top-looking for me.

Btw…in my opinion, the need to have some sort of understanding of the explosive growth in Top Glove is kinda important.

So far, it looks to me it has been 'quite' prudent in the number of factories it has been adding per year. Yes, adding a new factory per year is indeed aggressive but i think it has not been too aggressive. (tiok boh?) From a management point of view, consideration should be given regarding the ability for Top Glove to manage the growth in its factories. (Layman's view: Buying and managing a business is always manageable, but if u buy 'too much' businesses, then the very obvious issue, is can we manage all these factories?) Yup, the issue of managing and cordination of all factories in a profitable and efficient manner becomes a concern if the company increases the number of factories too fast.

Whereas, the increment in production line should be a much easier task to handle compared to the number of factories. (tiok boh?)

Now one probably ask why all this? Growth in a company is always good however commonsense would tell us that excessive growth might pose some danger too. As such, this is why I am not discounting this issue.

Which is what is happening in Top Glove isn’t it? The company is expanding and expanding and expanding. Buy/adding a new factory here and there… but all these capex comes with a huge borrowing cost… and in me opinion…i the end result just does not justify all these expansions. Take a look at their Thailand and China segmental results. Does it justify all the moola spend expanding into these markets?

How? What say u?

Am I too prejudiced against what Top Glove has achieved so far?

Is all my mumblings not valid? Or am I mumbling just for the sake of mumbling?

:D