* edited 5th April 2006 *

Past postings:

In the first posting, I wrote the following..

- However….what puzzles me is… where is ze Moola?

Mana pergi tok?

If i remember correctly, Jason Zweig stated somewhere (cannot remember which page lah) in the Fourth Revised edition of the legendary Benjamin Graham’s book, “The Intelligent Investor”…the best definition of a good business is that the good business generates more cash than it consumes.

The good business is generating more cash of the company’s piggy bank and the company’s piggy bank grows at a healthy pace.

Think about it.

Isn’t this what we want for our investment?

Now if a company keeps growing in size and expanding and expanding….sales is growing lah, net earnings is also growing at a fantastic rate….but then... somehow the end result is not there.. cos the company’s piggy bank is NOT reflecting the excellent result. Yup, company sales are increasing, net profits are increasing BUT cash is depleting. And in some drastic cases, the company’s loans are increasing too.

And this is my current prejudice against Top Glove.

Where is ze Moola?

Top Glove announced it MADE a net profit of 58.1 million for the current fiscal year 2005.

Fantastic! Bravo! Superb!

However.. open the company’s earnings excel file.. and look at the CF worksheet.

Line 41: Cash and cash equivalent at beginning of the year was 16.168 million

Line 43: Cash and cash equivalent at end of end of period was 4.616 million.

Ahem.

4.616 million wor… and according to the company it MADE 58.1 million. Isn’t the company consuming MORE cash than it generates? How? Would u justify Top Glove being a top business?

And Top Glove’s total borrowings now total 154 million. Errr… a year ago… how much ar?

Sooooooooooo despite it’s great sales and net profit growth… it’s bottom-line certainly ain’t too top-looking for me.

Btw…in my opinion, the need to have some sort of understanding of the explosive growth in Top Glove is kinda important.

So far, it looks to me it has been 'quite' prudent in the number of factories it has been adding per year. Yes, adding a new factory per year is indeed aggressive but i think it has not been too aggressive. (tiok boh?) From a management point of view, consideration should be given regarding the ability for Top Glove to manage the growth in its factories. (Layman's view: Buying and managing a business is always manageable, but if u buy 'too much' businesses, then the very obvious issue, is can we manage all these factories?) Yup, the issue of managing and cordination of all factories in a profitable and efficient manner becomes a concern if the company increases the number of factories too fast.

Whereas, the increment in production line should be a much easier task to handle compared to the number of factories. (tiok boh?)

Now one probably ask why all this? Growth in a company is always good however commonsense would tell us that excessive growth might pose some danger too. As such, this is why I am not discounting this issue.

Which is what is happening in Top Glove isn’t it? The company is expanding and expanding and expanding. Buy/adding a new factory here and there… but all these capex comes with a huge borrowing cost… and in me opinion…i the end result just does not justify all these expansions. Take a look at their Thailand and China segmental results. Does it justify all the moola spend expanding into these markets?

How? What say u?

Am I too prejudiced against what Top Glove has achieved so far?

Top Glove announced its quarterly earnings tonite.

Let's look at their cash flow...

how?

And again.. Where is Ze Moola?

Did Top Glove's cash flow improved?

Was my earlier concern still valid?

Take a look at their balance sheet...

See how the total loans have increased a lot?

Short term Loans is now 47.934 million. Long term borrowings is now 81.544 million and Top Glove has issued bonds amounting 70 million.

And how did their current Thailand and China plants results appeal to you?

And how would one evaluate the following past comment below?

- Which is what is happening in Top Glove isn’t it? The company is expanding and expanding and expanding. Buy/adding a new factory here and there… but all these capex comes with a huge borrowing cost… and in me opinion… the end result just does not justify all these expansions. Take a look at their Thailand and China segmental results. Does it justify all the moola spend expanding into these markets?

Am I Wrong?

Btw... Top Glove is now at 7.70.... and all this is a mere mumbling from me... i have no idea what the share will do... will the so-called improved earnings seduce some demand today? I have no idea dude...

2 comments:

Moola,

I know that u r a rare knowledgeable investor. All what U had mumbling so far sound pretty reasonable. But for Topglove, i am have a different perspective. (I also dont own this stock)

Strictly followed Ben Graham, "a good company is a company made more money than it spend", i have no objection to this. But, sorry to say that this statement is too general. Stocks are different from each other, we cannot apply this rule across the board. On the Topglove case, i am of opinion that a good company should employ the profit/equity wisely, either thru' business expansion or returned to shareholders. I personally prefer business expansion. Pertaining to debt, a am of the opinion that some manageable debt is acceptable. Of course borrowings come with a cost. I do agreed with U that the pace Topglove is expanding is to fast.

2nd brother

Hello 2nd Brother,

Many thanks for the kind words.

I do hope that you understand that in the share market opinions and views will always differ.. so I do think there is no need for you to to be sorry that your opinion differs, ok?

You see, yes I do agree very much that a good company should employ their profit/equity wisely, which as you have said, either thru business expansion or returning the excess cash back to the shareholders.

And this is the very issue here in Top Glove.

Is Top Glove expanding their business wisely?

Take a very good look at their cash flow.

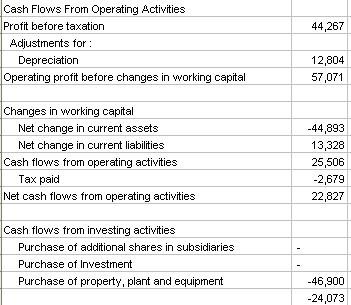

Based on current numbers... Top Glove recorded a record half year earnings of 38.360 million.

And the very same question I asked back in first posting in Oct 2005, I asked again yesterday, where is the Money? Where is the wealth generated?

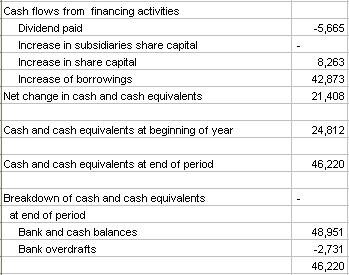

In this quarterly earnings, Top Glove mentioned that it's piggy bank cash at the start of the year was 24.812 million. At the end of this quarter, yes cash increased to 46.220 million BUT this was aided by an increase in borrowings of 42.873 million. If you minus out the borrowings, where did that earnings of 38.360 million go? And what if you take into consideration of the depreciation charges of 12.804 million?

Should one be worried that in Top Glove example, we are seeing a company that has been constantly consuming more cash than it generates?

And then what about the end results from Thailand and China?

And asked in the blog postings: 'And how did their current Thailand and China plants results appeal to you?'

Now these are the issues I have raised...

What's one opinion on it?

Do you agree or do you disagree?

For some.. they get worried... company cash flow has not been positive for a long time already, so is it wrong to be worried? Is the justifications to be worried valid?

However... ahhh... the differing opinions.... :D

For some.. it is considered OK.. since they consider that because Top Glove is expanding and has the inspirations to be the TOP GLOVE MAKER in the world. And to be no.1, some sacrifices needs to be made. The company has to use their cash flow to fund the expansions. And if that is not enough, the company has to borrow more to fund the expansions.

Ahh... do you see the differing opinions?

Which is right?

Which is wrong?

I have no idea... me just raised the issues only via my mumblings...

Post a Comment