Adventa announced its earnings today.

Before I opened the earnings, I remembered an article on the Edge Financial Daily: Delay in Adventa’s expansion plan. It's written by RHB Research.

- Maintain outperform at RM3.14 with fair value of RM5.19 (from RM4.34): Adventa is due to announce its 2QFY10 results today.

We expect Adventa to post a low double-digit year-on-year (y-o-y) revenue growth largely due to a combination of higher volume sales as a result of expansion in capacity which came on-stream in the later part last year.

This however would be offset by the higher raw material costs as latex price rose 62.7% (y-o-y) and weaker US dollar (-7.4% y-o-y) against ringgit and as a result, core earnings could be flat y-o-y.

Quarter-on-quarter (q-o-q), revenue is expected to be higher by a mid-single digit mainly due to higher selling prices in order to pass on the higher raw material costs to customers.

However, we believe the increase in selling prices would not be enough to offset the higher raw material prices (+24.8% q-o-q) and weaker US dollar (-2.5% q-o-q) due to the time lag in passing on the higher cost. Consequently, we expect 2Q10 net profit to be lower q-o-q.

Management has guided that the commercial production for its new factory in Kluang, Johor has been delayed due to the delay in shipment of some parts for the lines by the supplier.

Following that, in 2011, the management plans to add another five double former lines, which will increase Adventa’s annual production capacity for dental and examination gloves to 5.5 billion pieces by end-2011 from 4.5 billion pieces at end-2010.

Capex (capital expenditure) guided by management is RM30 million per year which will be funded internally and via borrowings.

The risks include: 1) sharp surge in latex price which may result in margin squeeze; 2) an appreciating ringgit against the US dollar and 3) execution risk from its capacity expansion.

We have lowered our FY10-11 revenue projection by 1.2%-1.5% after factoring in the slight delay in the expansion plan. At the same time, we have also lowered our FY10-FY11 Ebitda margins assumptions by 1.1-1.2 percentage points to reflect the time lag in passing on the cost increase to consumers.

As a result, our FY10-11 earnings forecasts have been lowered by 6.7%-8.3%. We maintain our FY12 earnings forecasts for now.

Despite the cut in our earnings forecasts, our indicative fair value has been raised to RM5.19 as we roll forward our valuation year to FY11 (from RM4.34 based on CY10). No change to our target PER of 13 times and outperform call on the stock. — RHB Research Institute, June 14

Well, it's pretty much spot on.

Adventa earned 6.450 million for the current quarter, fy 2010 Q2. Half year net earnings came in at 15.803 million.

Adventa's earnings of 6.450 million was much better than it's 3.789 million on a y-y comparison. And on a q-q comparison net earnings, the previous quarter, Adventa reported net earnings of 9.353 million.

The weak numbers are as expected but it looks much weaker than what RHB had expected. RHB's fy 2010 estimate earnings for Adventa are 41.9million. Adventa only did 15.803 million for first half of 2010.

I then took a look at Adventa's balance sheet to look see. Yeah, I wanted to see how it measures up.

I was not too impressed.

So RHB had said that Adventa management had guided that capex would be around 30 million.

Cash and bank balances did showed decline when compared to previous year.

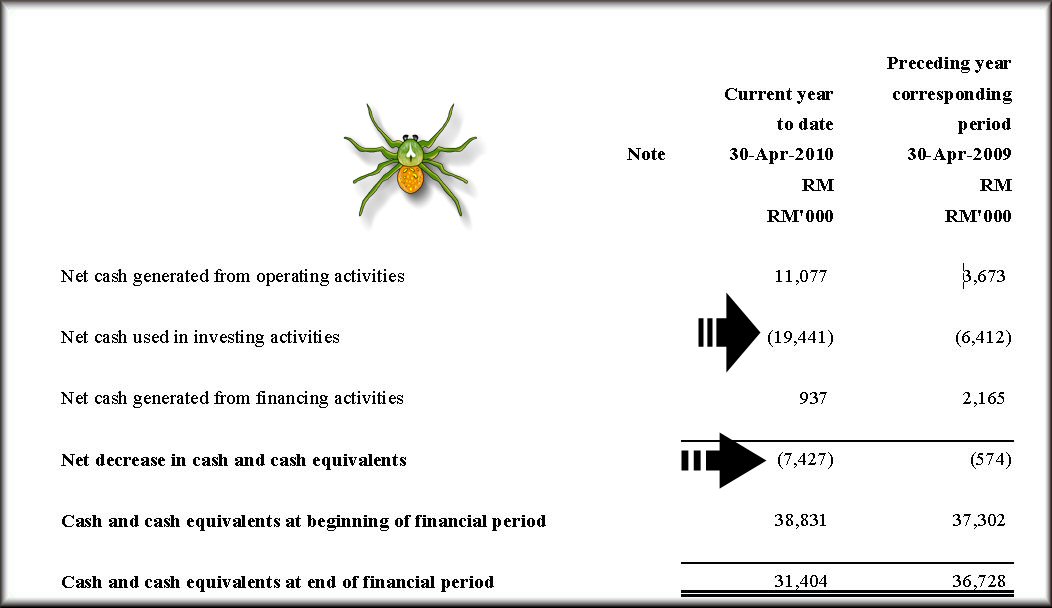

I then wanted to see the cash flow statement.

Arrrggggggrhhhhhh..... as you can see from the above, it's a summarised cash flow statement.

Argggghhhhhhhhhh!

That's it.

I lost all interest in the stock.

Yup. No more interest at all. I cannot see the point at all when the company chooses not to be transparent with its cash flow statement.

Hey, less one 'investment grade' stock to watch won't hurt me at all.

(ps: the issues causing the lower Adventa's earnings is a concern for the rest of the glove sector, yes? )

2 comments:

Hmm..Perhaps the company decided to cut cost by eliminating the details in cashflow but I thought companies in general dont go into detail in interim reports...

JP: LOL! Don't get me wrong, I am not suggesting anything. Thie is just a rather simple posting to share. For me, given the choice, I might just 'avoid' Adventa for the reason I mentioned in the posting. That's all. :D

Post a Comment